Your Healthcare Insurer Is Plenty Profitable (shh...don't tell the regulators)

Another installment of "Don't Hate Your HMO - Invest in It!"

Managed Care Organizations, or MCOs, are the health insurance companies in the U.S. These are companies Aetna, UnitedHealth, and the Blue Cross Blue Shield companies unique to each state market.

And, they are a lot more profitable than meets the eye.

People just love to hate their MCO. The reason is simple – MCOs are the middlemen between insatiable demand and limited supply.

In the U.S., the MCOs are the part of the healthcare system that says “No”. When dealing with our health, no one wants to hear “no”. That’s because health is the #1 asset we own. Without your health nothing else matters.

This was put on tragic display last Fall when the CEO of UnitedHealthCare paid the ultimate price of a gunman’s frustrations with health insurance companies.

Unfortunately, MCOs are good at saying no even when they should be saying yes. Automated claims systems are programed to find the tiniest of mistakes to reject a claim. New AI systems are taking it even further to deny claims based on a certain set of circumstances driven by an algorithm.

It is maddening to deal with when this happens and easy to see why most people despise their health insurers.

That said, the stocks of these companies have been great investments for a number of reasons. For more details see my report “Don’t Hate Your HMO – Invest in It!”

When MCOs get in trouble for denying too many claims, one of the “go-to” arguments from management is “We are not making a lot of money. We are a low profit business.”

From a textbook accounting perspective that is true. Most MCOs report single-digit net profit margins. However, a major part of that “low profitability” is related to the fact that MCOs pay for healthcare and therefore drive big revenues.

Remember, MCOs are in the business of paying for medical bills. In the U.S., this is a $5 trillion powerhouse industry. Therefore, MCOs must price their “product” to capture the expected medical costs of their members.

All of this spending becomes revenue for the MCOs even though they don’t get to keep much of it. And as we all know, healthcare costs rise 7%-9% per year consistently. These businesses get to raise the price of their product every year to meet this rise in underlying costs.

At the end of the day, the MCOs collect expected medical spending as part of their premium revenue and then pass most of it to doctors, hospitals, labs, imaging centers and other providers as their biggest operating expense. As a percent of revenue, medical expenses are roughly 85%.

In essence, MCOs are merely transaction processors. They evaluate healthcare claims of their members and then pay the doctors for the service. Medical expenses are a “pass-through” meaning they simply flow through the business. On the income statement, medical expenses run into the revenue line, and then out the medical expense line.

Let’s ask a question. What would MCO profit margins be if we pulled medical costs from both the revenue line and the expense line and redid the math of the profit margin?

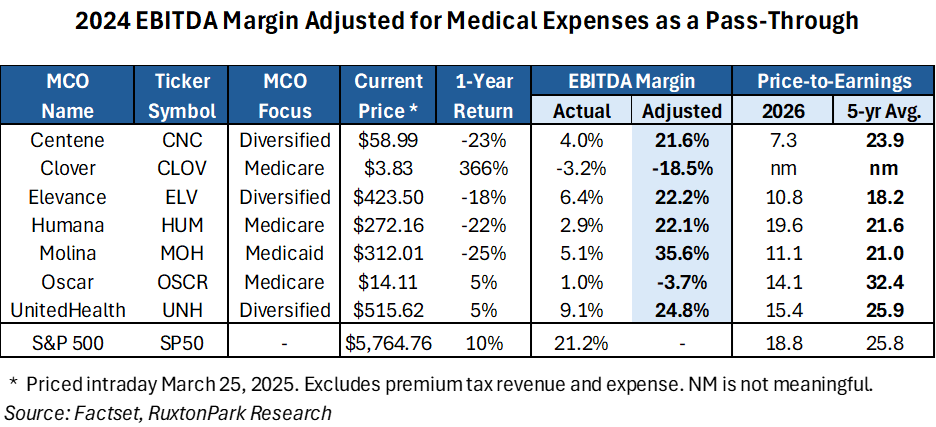

In the table below, we adjust 2024 income statements by removing medical expense from both total revenue and operating expenses and then recast the profit margin. In our analysis we use EBITDA (earnings before interest, taxes, depreciation and amortization) as the measure of profitability. This adjusts for financing and tax policy differences when comparing one company to another. We also reduce investment income as the MCOs would have less revenue to invest for gains. Important to note - this analysis is not without flaws but serves to demonstrate the magnitude of profit difference if medical expenses were not considered part of the accounting.

In all but a two cases, EBITDA margin is substantially higher than what is reported by the companies.

Look at UnitedHealth, the MCO that is catching a lot of heat right now for denying too many claims. If medical expenses are considered a “pass-through” and therefore ignored on the income statement, EBITDA margin is almost 25% in 2024.

Or take Molina Healthcare, a government-focused MCO that pays the medical bills for people on Medicaid and the health insurance exchanges. If we evaluate its profitability without healthcare costs as part of revenue and expenses, EBITDA margin is 7x higher. At 35%, Molina is right up there with tech giant Apple. It also realized 35% EBITDA margin in 2024. That’s crazy, right?

Crazy as it may be this little-discussed characteristic of MCOs makes them very attractive investments.

Furthermore, these stocks are trading at 2026 P/E ratios well below their five-year averages.

Considered best-in-class UnitedHealth trading at 15x versus a 25x average over the prior five years. Or Centene trading at only 7x vs about 24x. Both are currently cheaper than the S&P500 as a whole.

During my time as a healthcare analyst, I often wondered why investors didn’t pay more attention to this characteristic. It is a great consideration for fundamental investors.

The major risk is that regulators will catch on to this and create legislation to tighten profits. However, in our view this risk is tiny. A change like this would require another round of comprehensive healthcare reform. That is nowhere to be seen right now and would take years to design, become law, and implement.

These are great stocks with strong operating margins trading at really reasonable prices.

Furthermore, they are defensive and should do well if the U.S. plunges into recession. Most major U.S. banks are now saying recession is 40%-50% probable. Time will tell but in our view it makes sense to own some of these stocks or a healthcare ETF like the Health Care Select Sector SPDR Fund, ticker XLV.

RuxtonPark Research prefers Centene, Humana, and UnitedHealth as its MCO investments of choice and owns them all for the long term.

As we like to say, “Don’t hate your HMO – Invest in It!” (and don’t tell the regulators).

Cheers,

Thomas Carroll

Founder, RuxtonPark Research

Important Disclaimer. Nothing in this report or anything written by RuxtonPark Research, Thomas Carroll, or affiliated research should ever be considered individual investment advice. This is purely for information and educational purposes only. Every investment involves risk, and participants should do ample due diligence, seek the counsel of registered investment advisors, and only risk what they can afford to lose.